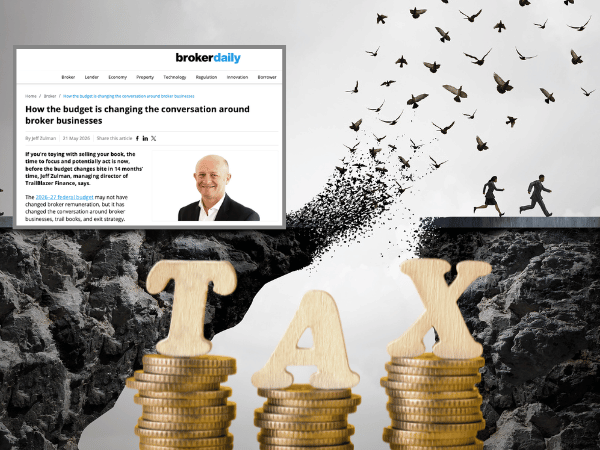

Trailblazer Finance values what traditional lenders overlook, we know the value of your recurring income! TrailBlazer offers flexible repayment options, competitive rates, quick approvals, and a personal touch to help your business thrive. Experience finance solutions tailored to your needs.